08 Dec The Fine Wine Market in 2021

by Liv-Ex

Introduction

All previous records set in 2020 have been broken and surpassed in 2021, marking the most successful year ever for the secondary fine wine market.

Fine wine trading continually broke new ground in terms of the value of wine traded and the sheer breadth of wines now active in the market. The industry benchmark, the Liv-ex Fine Wine 100 index (which tracks the price performance of the 100 most-traded wines in the secondary market), reclaimed and then exceeded its decade-old former peak, while the Liv-ex Fine Wine 1000 rose for 18 consecutive months.

Fine wine collectors returned in force to classic labels and regions, even as the market base continued to broaden and diversify.

On the surface, this year appears very simple. As our accompanying charts show, the entire direction of the market has simply been… up. But there’s much more to it than that.

The recent publication of the 2021 Liv-ex Power 100 explained many of the reasons behind this year’s results. After a challenging start to 2020, the impetus from the latter half of last year continued, unabated, throughout this year.

The legacy of accumulated savings from the 2020 lockdown and low-to-zero interest rates continued to drive investment in alternative assets. Even when lockdown measures largely eased, fine wine remained in the spotlight.

One important change was the end of US tariffs on European wine imports. Suspended in March and formally abolished in June, this brought US buyers back to replenish their supplies of Bordeaux and Burgundy, providing both regions with demand that was largely denied to them in 2020.

This helped redress the balance of the market after last year’s surging performance from Italy, California and the Rhône but did not stop the market from continuing to broaden and diversify.

On the one hand, brand new wines from non-mainstream countries and regions (Lebanon, Austria, Armenia) traded for the first time. On the other hand, trade deepened within established categories such as Burgundy, Italy and California.

Many may have hoped that 2021 would be the year when our societies broke free of Covid-related restrictions and discussions. As the year draws to a close, it is clear that we are not quite free of it yet.

Nonetheless, with a continued lack of clarity surrounding the future, enthusiasts, collectors, and investors have continued to trust in the steady returns and gustatory pleasures of fine wine.

It remains to be seen if this bullishness will survive the likely return of tighter fiscal and monetary conditions.

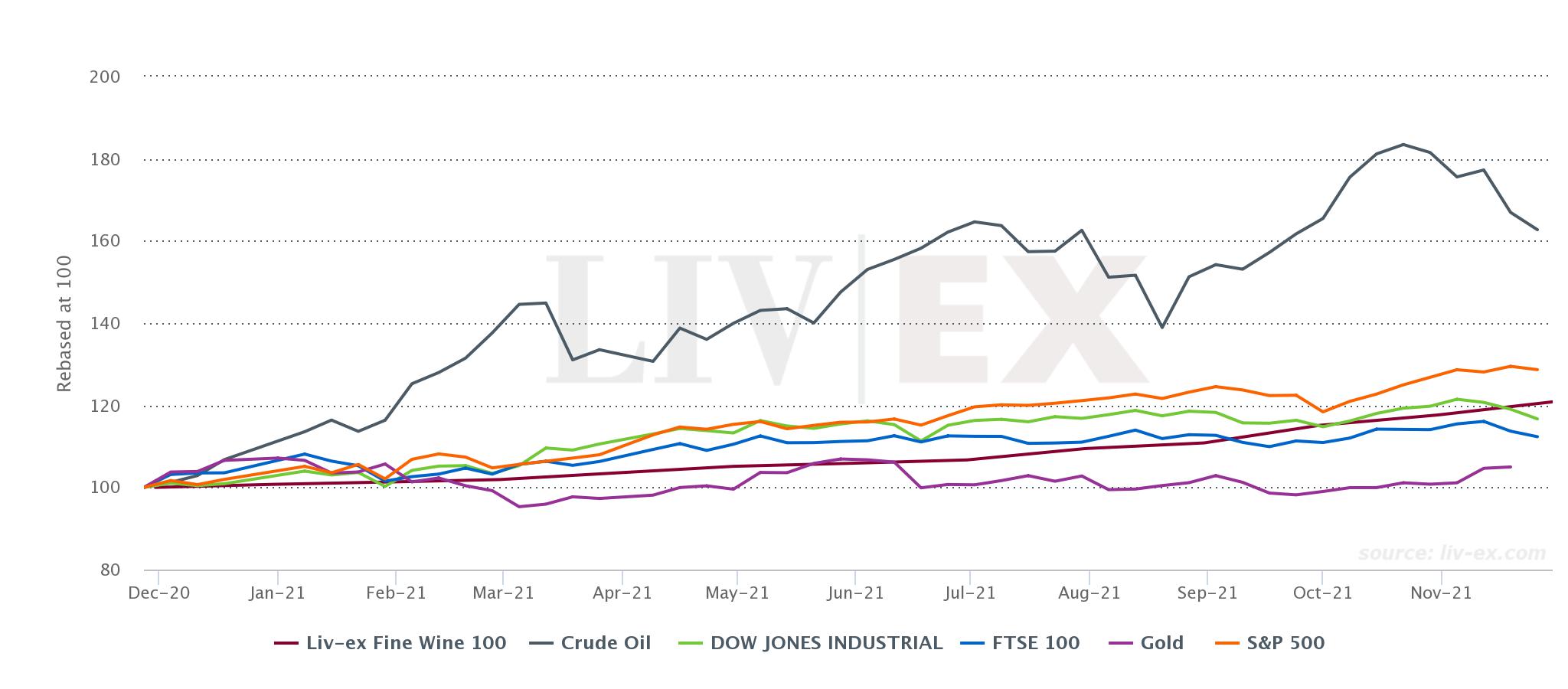

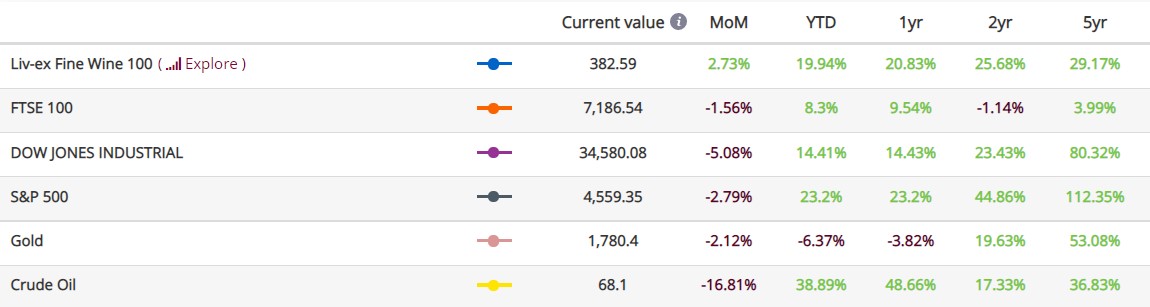

Fine wine outperforms equities

– Current value as of 6th December 2021.

Over the last year, fine wine (as measured by the Liv-ex Fine Wine 100 index) has been a better investment than several traditional equity markets, including the FTSE 100, Dow Jones and gold.

The Liv-ex 100, 1000 and 50 indices, have risen every month this year. Both the Liv-ex 100 and Liv-ex 1000 have now enjoyed 18 consecutive months of positive progress.

– Current value as of 6th December 2021.

What’s driving fine wine prices?

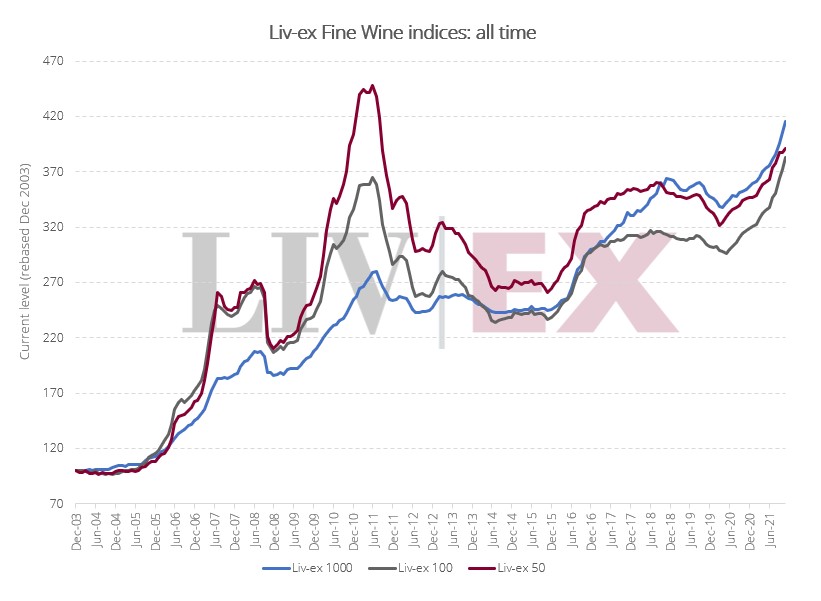

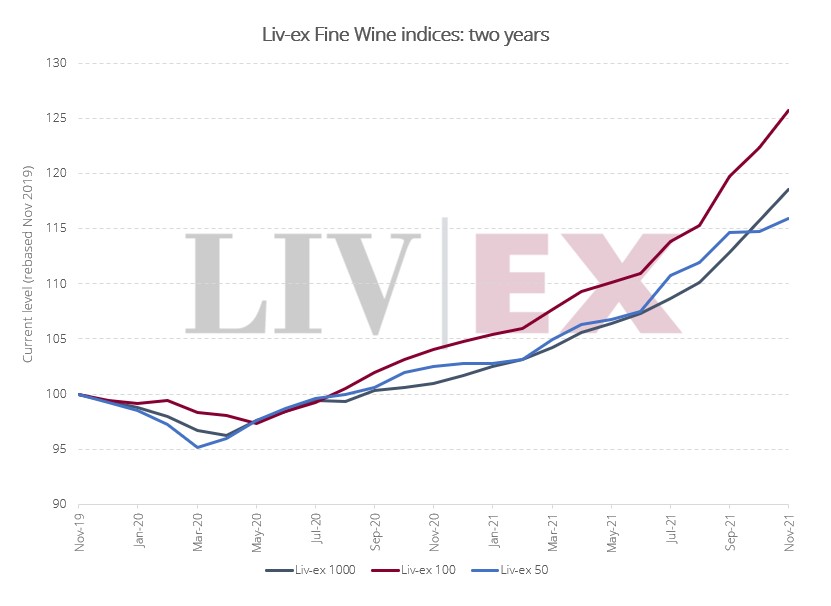

As the market broadens and prices rise across a greater variety of labels, it is no surprise that the broadest measure of the market, the Liv-ex 1000 index, has started to emerge as the top-performing of the three indices.

As the chart above shows, the Liv-ex Fine Wine 1000 index – which tracks the price performance of 1,000 wines from across the world – is up 315.3% since inception. By contrast the Liv-ex 100 and Liv-ex 50 are up 282.5% and 290.4% respectively.

This does not quite tell the whole story, however. It is in fact the Liv-ex 100 which has been quietly out-performing the Liv-ex 1000 and Liv-ex 50 over the last two years, as shown in the chart below.

The benchmark index not only returned to the peak it achieved in 2010-11 at the height of the China-driven bull run, but it also surpassed it in October.

Even as equity markets were rocked in November after the news of the new ‘Omicron’ variant, the Liv-ex 100 rose 2.7%.

The performance of the Liv-ex 100 is a testament to the rising prices at the very top end of the market. With blue chip Bordeaux and most especially Burgundy back in vogue, the benchmark index is hitting its stride once again.

The Liv-ex Fine Wine 50, which tracks the performance of the First Growths, is rising more slowly than the Liv-ex 100 and Liv-ex 1000. The Liv-ex 50 rose the highest during the 2010-2011 bull market and is the only one of the three indices not to have returned to that former peak.

This is because the price-performance of individual vintages has not been as dynamic, despite the total value of First Growths traded this year being very high.

Therefore, although the First Growths are among the top traded wines by value this year, neither the Liv-ex 50 nor the broader Bordeaux 500 indices, have been reclaiming old records or out-performing their peers.

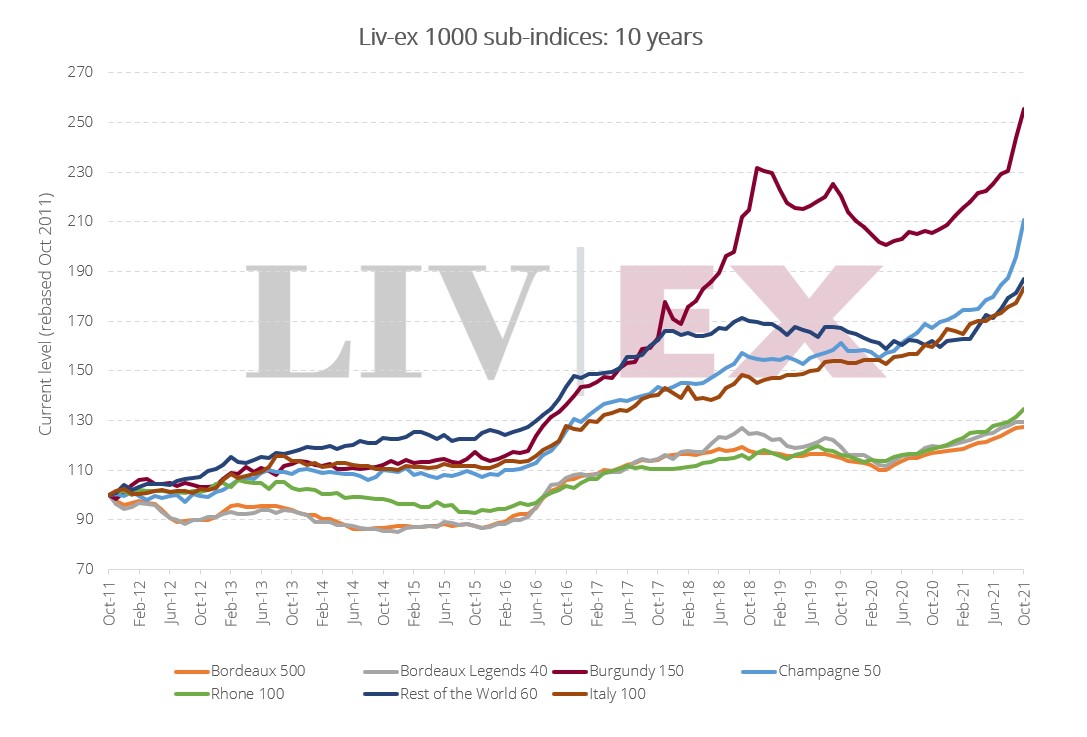

The broader market’s performance

While blue chip labels are contributing to the rise of the Liv-ex 100 index, the Liv-ex 1000 is also flourishing as the market continues to expand.

All of the sub-indices in the Liv-ex 1000 have risen this year. The dip experienced in the first half of 2020 has been erased over the last 18 months and all the indices are positive over the year-to-date, one year and two year stretches.

Of the Liv-ex 1000’s sub-indices, the weakest performer has been the Bordeaux 500. The sub-index is up 9.2% year-to-date, while the Champagne 50 has been the best, rising 33.7%.

The performance of Burgundy has been noteworthy too. Up 27.1% this year, prices for the region’s leading labels have pushed on once more. Several vintages of Domaine de la Romanée-Conti hit new all-time highs earlier this year, while grand cru wines from the likes of Armand Rousseau and Domaine Leflaive have been among the year’s best-performing labels.

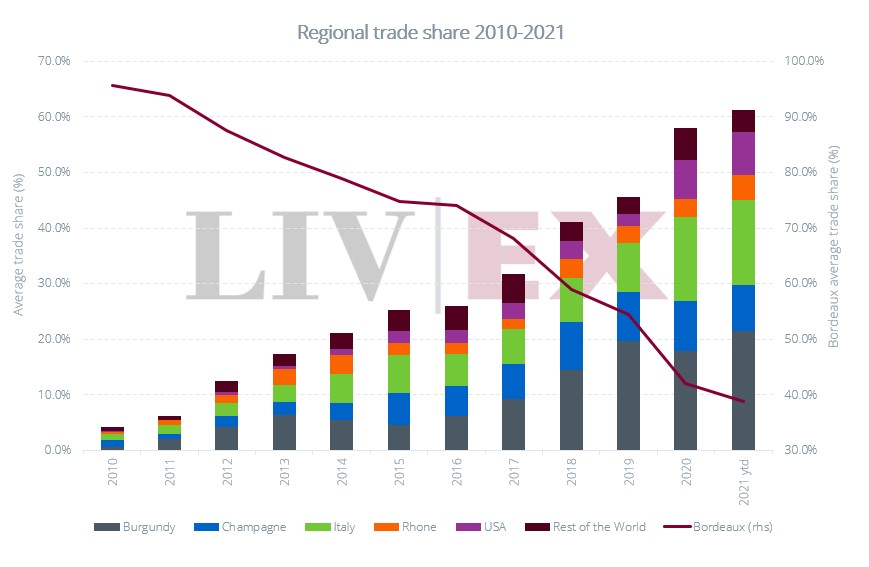

Bordeaux trade falls to new low

When looking at the breakdown of secondary market trade by region, 2021 saw the continuation of Bordeaux’s declining trade share. At the end of 2020 the region’s share of total trade (calculated as a percentage of total value traded) was 42% but that fell to 38.8% this year – a new low.

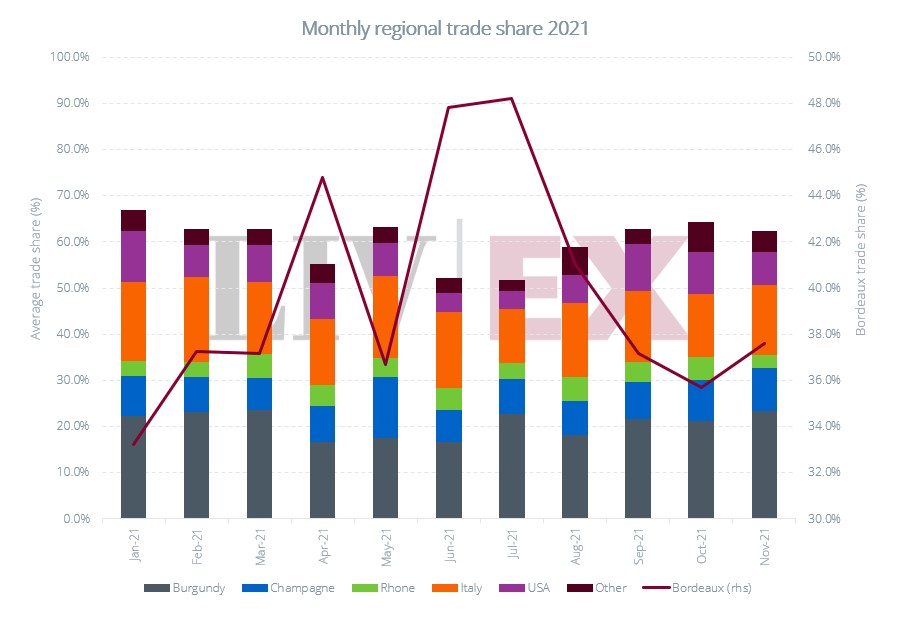

Forty percent felt an appropriate level for what remains an extremely important component of the secondary market. However, on its current trajectory, it is possible that this share could decline further as buyers focus on a smaller handful of leading châteaux. Nonetheless, as the chart below shows, activity did rise substantially over the summer when the 2020s were offered En Primeur.

Burgundy meanwhile reached a new all-time high. Its share of trade this year was 21.4%, beating its previous record of 19.7% in 2019. The Rhône and US had record years too, with respective shares of 4.5% and 7.6%. Italy stayed steady at 15.3%, a very slight increase from its 15.1% record last year.

Despite an astonishingly positive year in terms of price performance, Champagne saw a slight decrease in its trade share, down to 8.4%.

More wines trade on the secondary market than ever before

The number of producers traded on the secondary market this year hit 4,411, 7.6% higher than in 2020. While the number of wines traded reached 11,452, 10.5% more than in 2020 and almost seven times higher than a decade ago.

The fine wine market is certainly moving beyond just Bordeaux, which has been best demonstrated in the regional trade share chart above.

Wines from various winemaking regions, large and small, now trade on the secondary market – from Spain’s Balearic Islands to Aconcagua in Chile, and from the Palatinate in Germany to Calabria and Campania in Italy.

Non-traditional wine regions such as these are gaining momentum at the expense of the established forces that shaped the market in its first decades.

Though numbers remain tiny in comparison to more established fine wine regions like Bordeaux and Burgundy, smaller regions have demonstrated potential for faster growth. One such case is the UK, which has more than doubled the number of wines and spirits traded on Liv-ex on last year (from 14 to 32).

This broadening of the market is not just across new regions but also within existing ones too. As recently explored, Burgundy has seen the biggest increase in wines trading year-to-date, as well as being the region with the highest number of wines trading.

Burgundy exemplifies the case of diversification within the region itself, as buyers seek value among different price tiers which enables new domains to enter the secondary market.

To calculate the number of brands and wines trading we use LWIN – the Liv-ex Wine Identification Number – is a universal identifier for wine and spirits. It’s a lot like ISBN for books. Each wine or spirit has a unique number which can be counted. By counting numbers rather than names, errors are reduced, and reporting is simplified.

Champagne’s best year to date

Despite a slightly diminished share of trade, 2021 has been an excellent year for Champagne. The Champagne 50 index is the best-performing among the Liv-ex-1000 indices with the leading price performers being Taittinger’s 2006 and 2008 Comtes de Champagne, Cristal Rosé 2008, Krug 2000 and Salon 2002, which have all risen in price by over 50% this year.

Indeed, the top price-performer this year was Salon’s 2002, which has risen 80% to £10,618 per dozen.

Only one Champagne in the Champagne 50 – Perrier-Jouët’s 2011 Belle Epoque – has turned in a negative performance this year.

The 2012 vintage has been the most-traded Champagne vintage, followed by the 2008. The late releases of Salon 2012, Krug 2008 and Dom Pérignon Rosé 2008 helped stimulate demand around wines from these vintages, which are already held high in critical esteem.

Rosé Champagne has been on the rise too. Although a small part of Champagne’s trade, now standing at 18%, it is becoming an increasingly relevant sub-category. Cristal’s 2013 and 2012 rosés have been among the top-traded Champagnes this year.

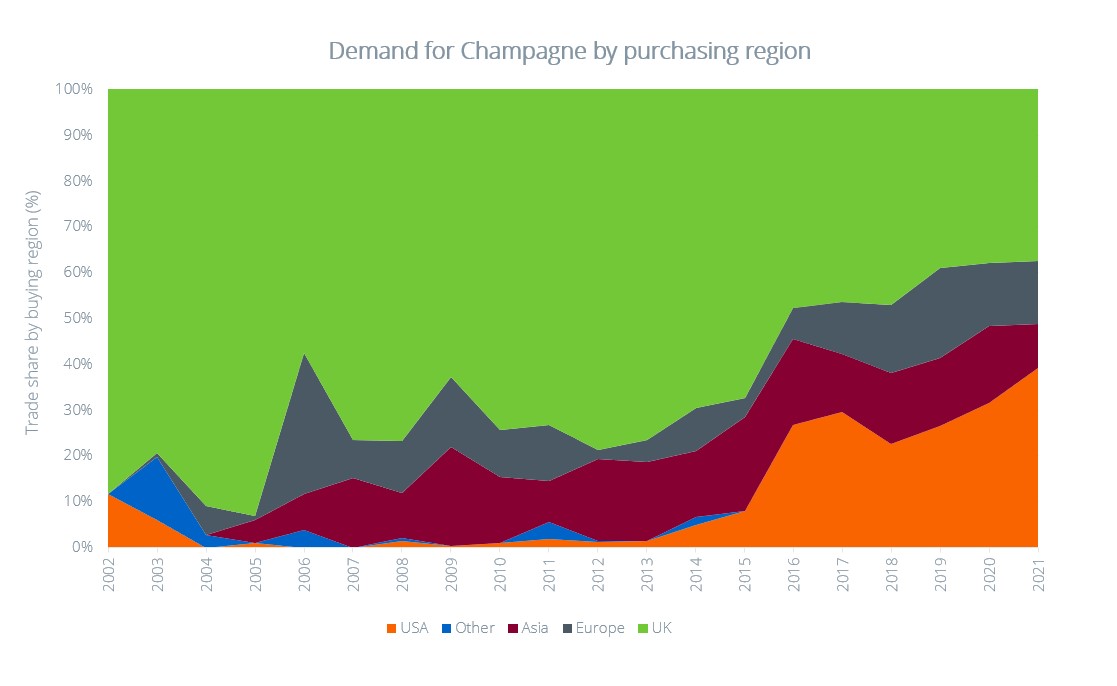

Market demand for champagne has also switched this year, as the US has overtaken the UK as the biggest buyer of Champagne on the secondary market.

US demand for Champagne rose in 2020 as it was one of the few regions exempt from the 2020 tariffs on European wines.

Since then, momentum has continued to build. Champagne sales to the US have risen 219% in 2021, as shown in the chart above.

The biggest price risers in 2021

Based on the wines included in the Liv-ex 1000 index using Liv-ex’s Mid Prices. For more information on Liv-ex’s pricing data, click here.

Based on the wines included in the Liv-ex 1000 index using Liv-ex’s Mid Prices. For more information on Liv-ex’s pricing data, click here.

Looking at the top price-performers this year, it is clear why the Champagne 50 and Burgundy 150 have been the leading Liv-ex 1000 sub-indices.

As mentioned above, Salon 2002 has led a near-universal set of rises across the Champagne 50 and is up 80.1% year-to-date. The wine has been traded actively throughout the year. It has been sought after since its release in 2017, but, now approaching its 20th anniversary, it has found some extra impetus.

Prices of DRC continue to climb though the biggest rises have been for its ‘other’ grands crus such as Grands Echézeaux and Richebourg, some of which have risen over 50% in price.

Domaine Leroy, not included in the Liv-ex 1000 due to its lack of liquidity, has likewise continued to see big rises across its range.

The rising demand and prices for these leading labels is continuing to have a knock-on effect for Burgundy’s remaining grands crus. Indeed, Armand Rousseau’s 2012 Chambertin was the second-best price performer (+73.6%), followed by Georges Roumier’s 2013 Bonnes Mares (69.1%) and Leflaive’s 2013 Bâtard-Montrachet (66.6%).

Beyond the big names we continue to see solid performances from other grand cru appellations. The Corton-Charlemagne from Bonneau du Martray and wines of Clos de Tart have also had a very positive year.

There is also the significant problem of supply. Rising global demand has coincided with increasingly small vintages in Burgundy. The harder they become to obtain, the more expensive many of these wines become.

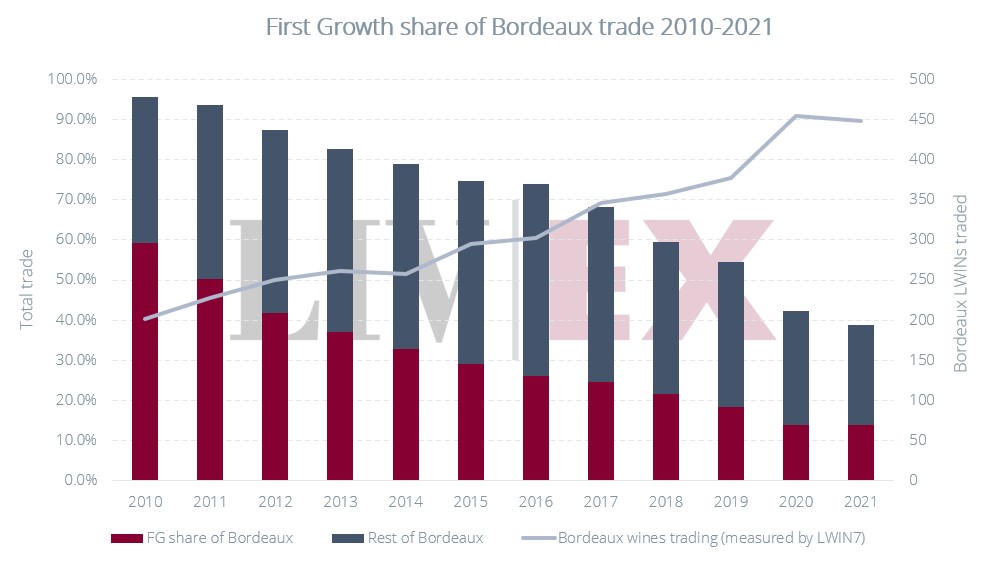

The First Growths’ share of Bordeaux trade rises

Bordeaux’s trade share continues to decline. Quite when or where it will stop or if it might even recover is hard to say.

With so many other wines clamouring for (and getting) attention from buyers, it is an increasingly competitive market for Bordeaux.

As the chart above shows, there is an increasing variety of Bordeaux wines trading but the majority of trade is focused around a few key estates – namely the First Growths.

These famous and desirable of Bordeaux estates have long been the backbone of the secondary market. At the time of the previous bull run in 2010, the First Growths accounted for 60% of Bordeaux trade by value (Bordeaux as a whole accounted for 95.7% of the market).

However, with the advent of anti-corruption measures in China in June 2011, this share fell to 53.5%. The combination of falling demand from China and an increasingly broader market has meant that the First Growths’ share of trade has fallen steadily since then. Last year the wines accounted for just 32.6% of Bordeaux’s trade.

But this year it has risen again and the First Growths’ share of Bordeaux trade went back up to 35.9%. Should the trend for Bordeaux buying continue to shrink, it’s possible that the First Growth’s share will grow.

Overall, the First Growths have had their best year since 2018, especially Château Lafite Rothschild which has been in high demand. The Chateau has been the most traded wine on the secondary market in 2021, as the table below shows.

However, what continues to hold Bordeaux back – even the First Growths – is price performance. Lafite’s 2011 vintage has been the best-performing red wine – up 32.5%. By comparison, the top five price risers this year had all returned over 66%.

The reasons for this are many but the continued withholding of stock from the market, especially at En Primeur, is stifling demand to some extent. A series of middling to poor En Primeur campaigns (despite some good recent vintages), also means what stock is out there is still readily available in many instances.

The top traded wines in 2021

The most traded brands are calculated by looking at the total value of each LWIN7 traded on Liv-ex. LWIN is the universal identifier for wine and spirits. LWINs are unique 7, 11, 16 or 18-digit codes. The 7-digit code refers to the wine itself (i.e. the producer and brand, grape or vineyard e.g. Lafite Rothschild). The longer codes include information about the vintage, bottle and pack size. To find out more, click here.

The successful year for the First Growths is highlighted by the top traded wines in the two accompanying tables.

Lafite in particular, which led the market a decade ago has bounced back as a leading label. However, as the progress of the Liv-ex 50 shows, impressive amounts of wine sold does not automatically equate to impressive price appreciation.

Sassicaia’s place on both lists is a further nod to the rising power of that particular Super Tuscan’s brand status.

The most traded wines are calculated by looking at the total value of each LWIN11 traded on Liv-ex. LWIN is the universal identifier for wine and spirits. LWINs are unique 7, 11, 16 or 18-digit codes. The 11-digit code refers to the wine and vintage (e.g. Lafite Rothschild 2018). The longer codes include information about the vintage, bottle and pack size. To find out more, click here.

Conclusion

It has been a strong year for the fine wine market. New records have been set for trade by value and volume and from a greater array of domains, châteaux and wineries than ever before.

The appetite for fine wine, whetted during the 2020 lockdowns, has not been slaked and whether for pure pleasure or portfolio diversity there has been no let-up in demand.

The combination of steady returns and low volatility, along with smaller yields and reduced stock availability from key regions, has enabled fine wine to prove itself a winning investment.

While the pandemic has, in its way, proved a boon to the market and while sentiment remains undeniably positive, no market rises indefinitely.

At the time of writing, for example, concerns over the new ‘Omicron’ variant have led to convulsions in mainstream financial markets; though this may prove temporary as its potential threat is assessed.

Although world events and macroeconomics may play their part in eventually blunting the market’s onward progress, it seems less likely that any reverse will trigger the sort of pull back seen in the summer of 2011.

The build-up to that particular peak a decade ago was marked by a mad scramble, with monthly rises of 2.7%, 3.1%, 5.5%, 6.1%, 4.3% and 2.8% between January and June 2010.

The current ascent, while impressive, has been much steadier, more deliberate, though it has picked up since July of this year. Importantly, the market is bigger and broader, no longer tied to the fortunes of a small set of wines. In 2019 when Burgundy went off the boil after a long stretch of extraordinary gains, the market soldiered on with barely a check.

Diversity is the market’s real underlying strength now and as buyers continue to understand that there are more wines to be discovered that solid foundation should prove invaluable.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £80m worth of wine and the ability to trade with 550 other wine businesses worldwide. They also organise payment and delivery through their storage, transportation, and support services. Wine businesses can find out how to price, buy and sell wine smarter at www.liv-ex.com.

Liv-ex Indices

Liv-ex’s indices are calculated using the Liv-ex Mid Price, which refers to the mid-point between the highest live bid and lowest live offer on the market. The prices are validated against additional data including transaction prices and are the most robust measure for pricing wines available in the market.

The reason for this is because other sources of fine wine price information and indices base their calculations on list prices. These are advertised prices, often collected from sellers who may be advertising wine that they don’t even have in stock. There is no firm commitment to buy or sell at an advertised price. The real value of the wine may be higher or lower than listed.

Liv-ex can uniquely provide prices from real transactions among the wine trade. These are historic trade prices, as well as firm commitments to buy or sell on the market at a given price. All transactions are standardised by condition and tax status, allowing you to make like-for-like comparisons. Our members value this because it is real, proven price information.